The 2021

Asset Allocation Index

PRESENTED BY

IN PARTNERSHIP WITH

The Canadian Leadership Congress is pleased to present the 2021 Asset Allocation Index, in partnership with Schroders. It’s our chance to check the pulse of Canadian asset owners and to take stock of their attitudes and intentions when it comes to their investments.

We sought to ask pension funds about their current allocations to equities, alternative investments, private markets, and ESG — and ultimately, what their intentions are for the future. Scroll down to find out what they’re thinking.

We sought to ask pension funds about their current allocations to equities, alternative investments, private markets, and ESG — and ultimately, what their intentions are for the future. Scroll down to find out what they’re thinking.

Key Highlights:

Drivers of asset allocation

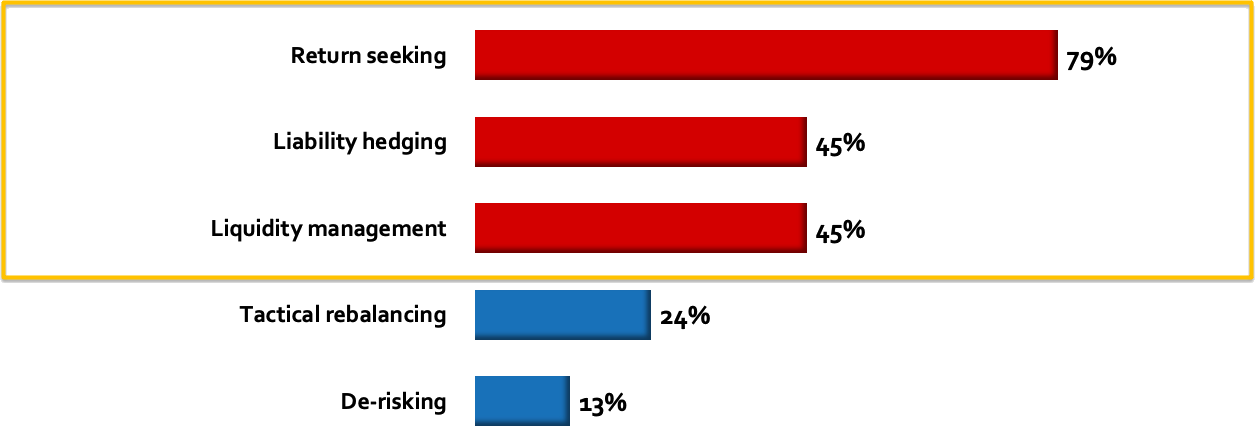

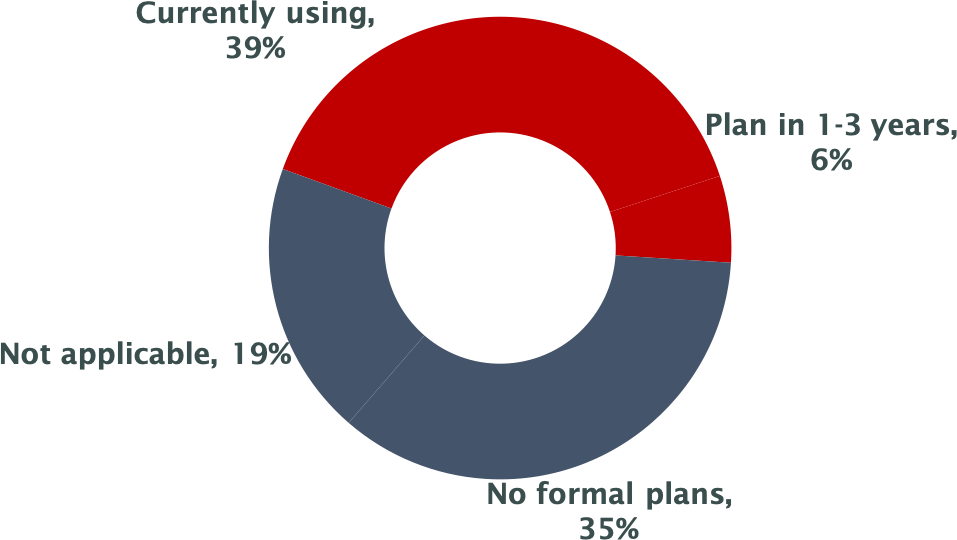

Not surprisingly given the pandemic, asset classes most likely to be causing concern are: public equities, real estate, domestic fixed income and global fixed income. At the same time, the top drivers of asset allocation are return seeking (79%), followed by liability hedging, 45% and liquidity management, 45%. Liability-driven investing is being used by just 39% of plans and, while 6% say they plan to start in the next 1-3 years, 54% say that they have no formal plans to use it (35%).

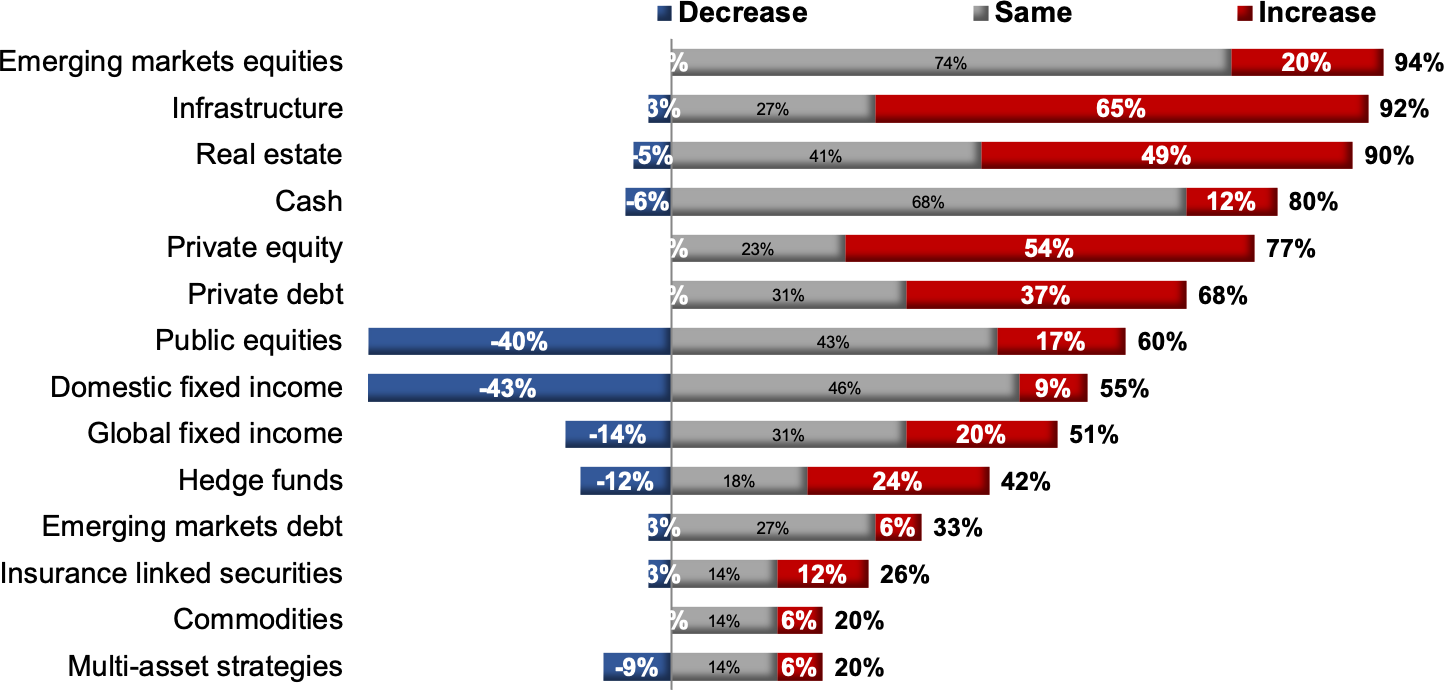

Looking ahead, respondents are looking to increase infrastructure, private equity and real estate while seeking to decrease domestic fixed income, global fixed income, and public equities. Private assets are on the rise — respondents are more likely to increase or maintain, not to decrease, their exposure.

Growth in private assets

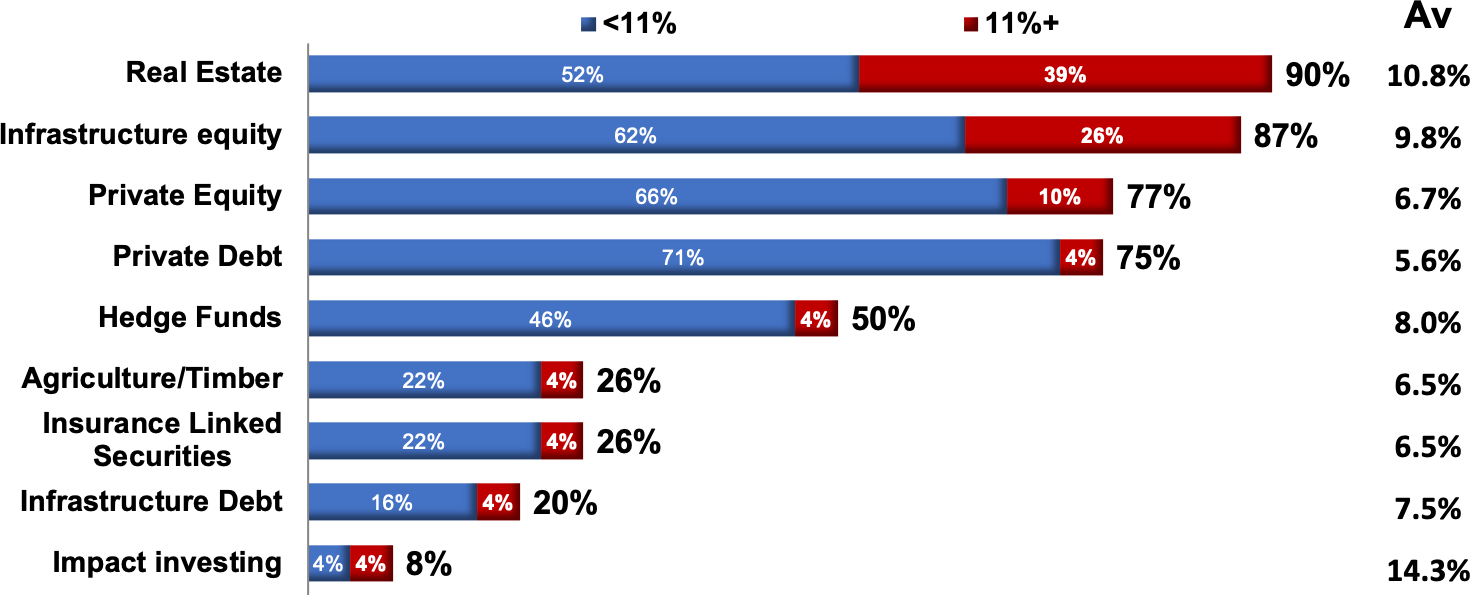

When it comes to private markets, the top holdings are real estate (90%), infrastructure equity (87%), private equity (77%), private debt (75%), and hedge funds (50%). Average allocations across our respondents include 10.8% of the plan for real estate, 9.8% for infrastructure equity, 6.7% for private equity, 5.6% for private debt and 8.0% for hedge funds.

ESG and implementation challenges

Over three quarters of respondents (78%) see ESG as important: 16% always, 35% currently and 26% struggling to implement it. Overall, however, 42% of plans have made changes related to sustainable investing with the most cited changes being Renewable energy investments/green initiatives, Global equity ESG, Fossil Fuel free.

It hasn’t always been an easy integration though — 87% of plans have faced obstacles when including ESG. Top challenges faced include difficulty comparing managers strategies, No historical return data, Not enough proof of return. Notably, no one identified high fees or lower returns as a challenge.

Drivers of asset allocation

Not surprisingly given the pandemic, asset classes most likely to be causing concern are: public equities, real estate, domestic fixed income and global fixed income. At the same time, the top drivers of asset allocation are return seeking (79%), followed by liability hedging, 45% and liquidity management, 45%. Liability-driven investing is being used by just 39% of plans and, while 6% say they plan to start in the next 1-3 years, 54% say that they have no formal plans to use it (35%).

Looking ahead, respondents are looking to increase infrastructure, private equity and real estate while seeking to decrease domestic fixed income, global fixed income, and public equities. Private assets are on the rise — respondents are more likely to increase or maintain, not to decrease, their exposure.

Growth in private assets

When it comes to private markets, the top holdings are real estate (90%), infrastructure equity (87%), private equity (77%), private debt (75%), and hedge funds (50%). Average allocations across our respondents include 10.8% of the plan for real estate, 9.8% for infrastructure equity, 6.7% for private equity, 5.6% for private debt and 8.0% for hedge funds.

ESG and implementation challenges

Over three quarters of respondents (78%) see ESG as important: 16% always, 35% currently and 26% struggling to implement it. Overall, however, 42% of plans have made changes related to sustainable investing with the most cited changes being Renewable energy investments/green initiatives, Global equity ESG, Fossil Fuel free.

It hasn’t always been an easy integration though — 87% of plans have faced obstacles when including ESG. Top challenges faced include difficulty comparing managers strategies, No historical return data, Not enough proof of return. Notably, no one identified high fees or lower returns as a challenge.

Key Drivers of Asset Allocation

Asset allocation is being driven by: Return seeking, 79%, followed by liability hedging, 45%, and liquidity management, 45%.

Asset allocation is being driven by: Return seeking, 79%, followed by liability hedging, 45%, and liquidity management, 45%.

Liability Driven Investing Importance

Overall, 39% of plans say they are currently using liability driven investing, with a further 6% saying they plan to start in the next 1-3 years. The remaining 54% say that they have no formal plans to use it (35%) or not applicable (19%).

Overall, 39% of plans say they are currently using liability driven investing, with a further 6% saying they plan to start in the next 1-3 years. The remaining 54% say that they have no formal plans to use it (35%) or not applicable (19%).

Planned Increase/Decrease to Asset Classes

Asset classes that are most likely to be increased in allocation are: Infrastructure, Private equity and Real estate. Asset classes that are most likely to be decreased in allocation are: Domestic fixed income, and Public equities.

Asset classes that are most likely to be increased in allocation are: Infrastructure, Private equity and Real estate. Asset classes that are most likely to be decreased in allocation are: Domestic fixed income, and Public equities.

Private Assets in Allocations

Overall, most plans include:

Overall, most plans include:

- Real Estate (90%) held with an average of 10.8% of the plan

- Infrastructure equity (87%) held with an average of 9.8% of the plan

- Private Equity (77%) held with an average of 6.7% of the plan

- Private Debt (75%) held with an average of 5.6% of the plan

- Hedge Funds (50%) held with an average of 8.0% of the plan

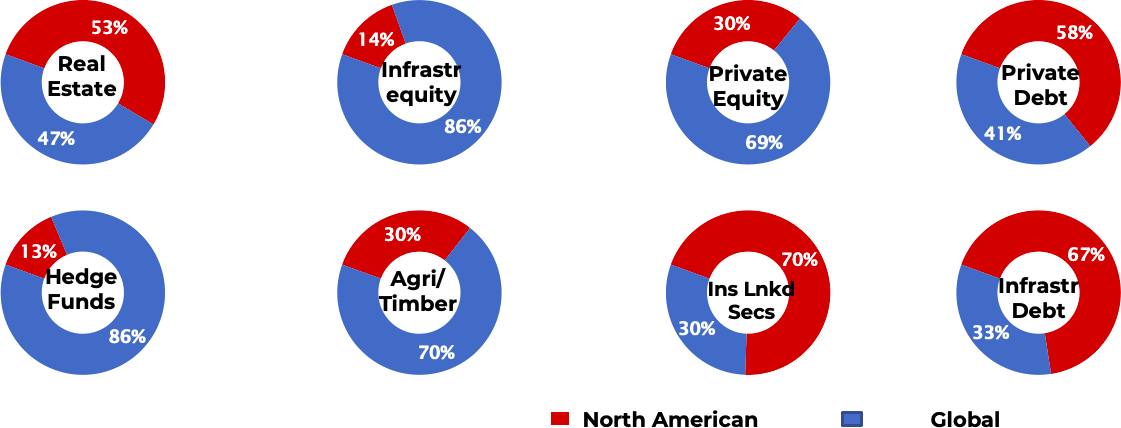

Private Assets North America vs. Global

For private assets, all plans selected either North American or global, no plan selected emerging markets for any of the asset classes. Among those who have holdings:

For private assets, all plans selected either North American or global, no plan selected emerging markets for any of the asset classes. Among those who have holdings:

- Real Estate holdings are split between North America and global

- Infrastructure is overwhelmingly global, 86% vs 14% North American

- Private equity leans toward global, 69% vs 30% North American

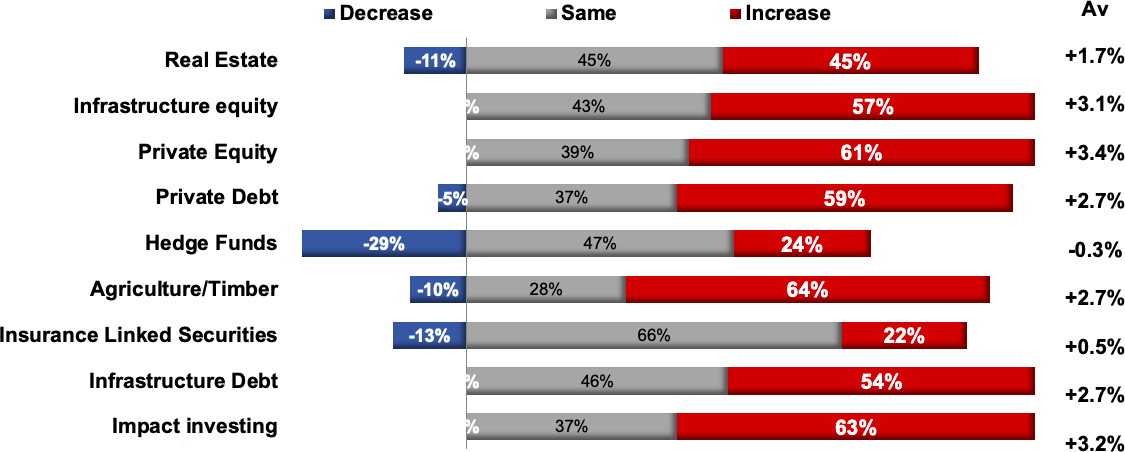

Allocation Changes to Private Assets

Of all of the private assets measured, plans are more likely to increase or maintain allocations than decrease. Notably highest for increasing are:

Of all of the private assets measured, plans are more likely to increase or maintain allocations than decrease. Notably highest for increasing are:

- Agriculture/Timber 64% of those with this asset plan to increase with a net average of +2.7%

- Impact investing 63% of those with this asset plan to increase with a net average of +3.2%

- Private equity 61% of those with this asset plan to increase with a net average of +3.4%

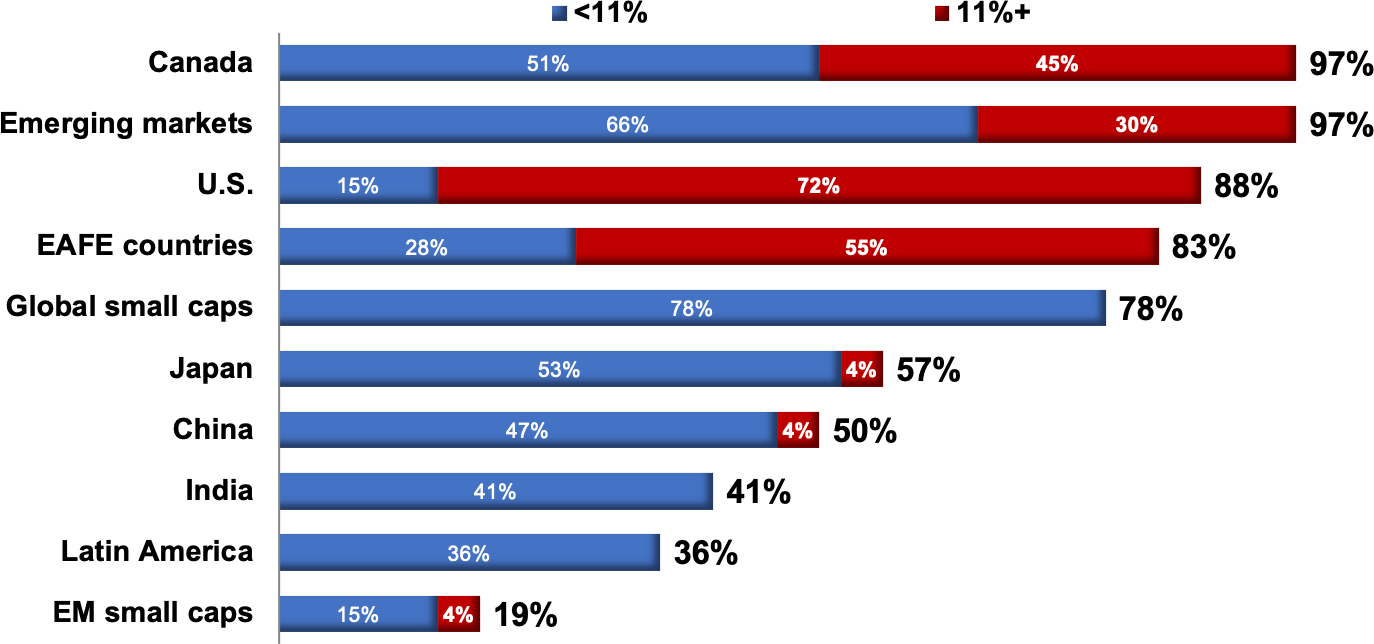

Equity Portfolio Allocations

Overall and nearly universally plans include:

Overall and nearly universally plans include:

- Canada (97%) held with an average of 11.9% of the plan

- Emerging markets (97%) held with an average of 9.8% of the plan

- U.S. (88%) held with an average of 19.5% of the plan

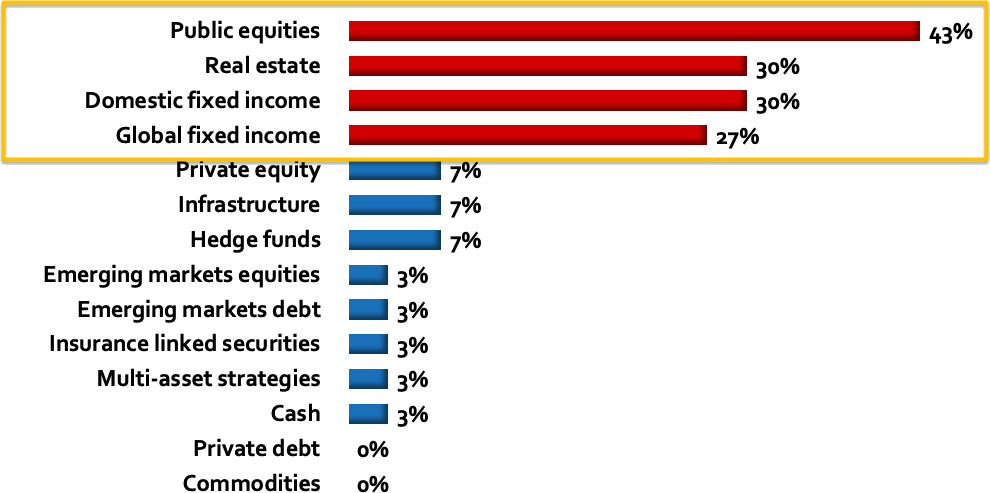

Asset Classes Causing Concern

Asset classes most likely to be causing concern are: Public equities, Real estate, Domestic fixed income and Global fixed income.

Asset classes most likely to be causing concern are: Public equities, Real estate, Domestic fixed income and Global fixed income.

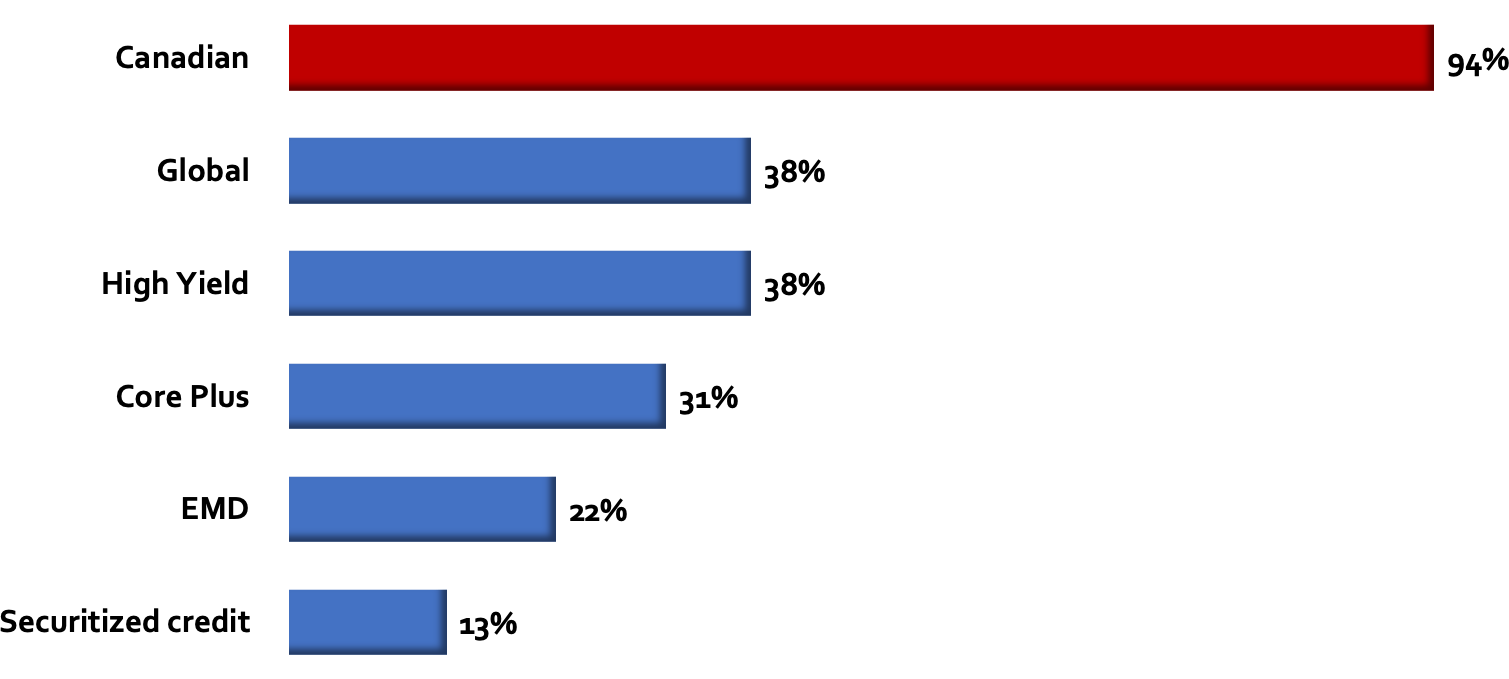

Allocations To Fixed Income Strategies

In terms of fixed income, Canadian is held nearly universally (94%). About a third hold Global, High Yield and Core plus fixed income strategies.

In terms of fixed income, Canadian is held nearly universally (94%). About a third hold Global, High Yield and Core plus fixed income strategies.

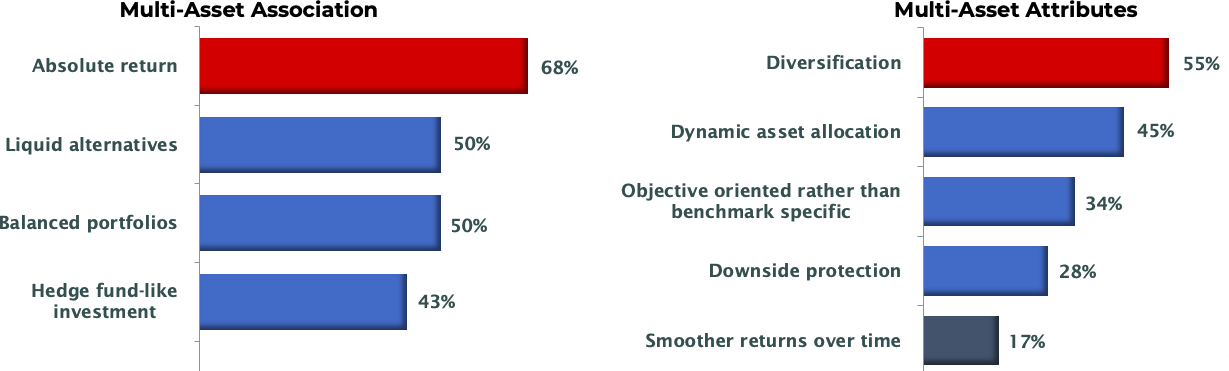

Multi-Asset Strategies

Multi-asset strategies are most likely to be associated with absolute return (68%) followed by Liquid alternatives and Balanced portfolios. The most cited benefits are: Diversification, Dynamic asset allocation and Objective oriented rather than benchmark specific.

Multi-asset strategies are most likely to be associated with absolute return (68%) followed by Liquid alternatives and Balanced portfolios. The most cited benefits are: Diversification, Dynamic asset allocation and Objective oriented rather than benchmark specific.

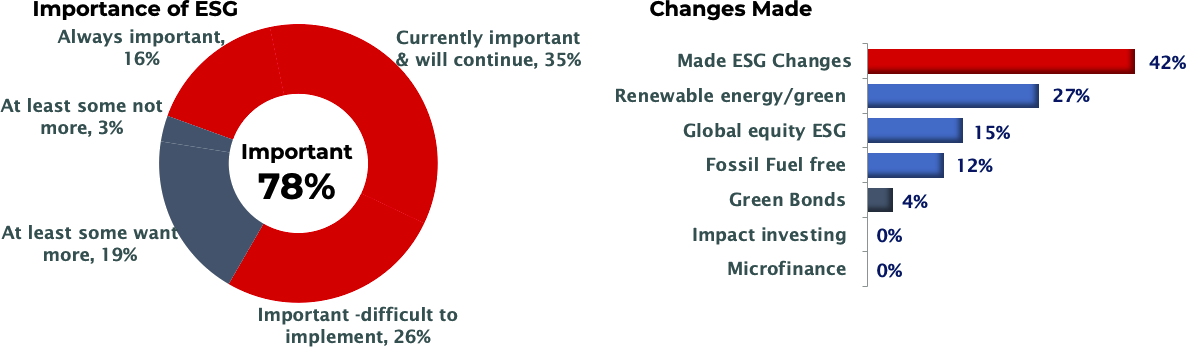

Importance of ESG

Over three quarters of plans (78%) see ESG as important: 16% have always seen it this way, while 35% say they currently view it this way. Nearly a quarter or 26% say they are struggling to implement. Overall, 42% of plans have made changes related to sustainable investing. The most cited changes are: Renewable energy investments/green initiatives, Global equity ESG, Fossil Fuel free.

Over three quarters of plans (78%) see ESG as important: 16% have always seen it this way, while 35% say they currently view it this way. Nearly a quarter or 26% say they are struggling to implement. Overall, 42% of plans have made changes related to sustainable investing. The most cited changes are: Renewable energy investments/green initiatives, Global equity ESG, Fossil Fuel free.

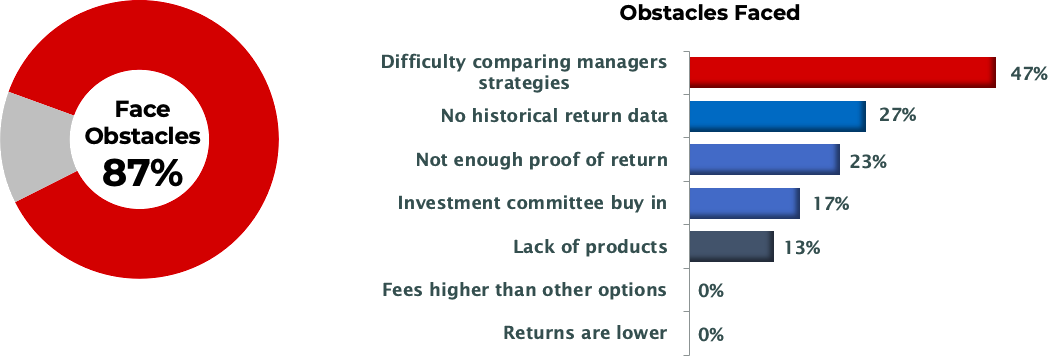

ESG Obstacles

87% of plans have faced obstacles when including ESG. The top obstacles faced are:

87% of plans have faced obstacles when including ESG. The top obstacles faced are:

- Difficulty comparing managers strategies, no historical return data, not enough proof of return

- Note that no plans identified high fees or lower returns as a challenge

IN PARTNERSHIP WITH